Government

About Finance

The Fiscal Officer and finance staff provide quality, transparent financial information to the Deerfield Trustees, residents, administration, employees and other external customers.

The Fiscal Officer is an elected official who serves independently from the Trustees. However, the Fiscal Officer must work closely with the Trustees assisting them in carrying out their legislative authority. The collective goal is to ensure that all decisions and actions comply with the laws and regulations of township governance.

The Deerfield fiscal office is responsible for the custody, investment, and disbursement of all township funds and follows the investment policy established by the Board of Trustees. The office has an obligation to insure that our records are as accurate as possible; therefore, the office takes the extra step of requesting an annual audit of our financial records.

The fiscal office works closely with the township administrator and staff in developing a budget that prudently uses the township’s financial resources. The Fiscal Officer and finance staff are constantly reviewing our processes in order to find cost-effective ways to enhance the financial services we provide for all our township residents and customers.

Since 2009, the fiscal office has published an audited Comprehensive Annual Financial Report consistent with state and federal requirements including Generally Accepted Accounting Principles (GAAP). The reports are available by selecting the links below.

Budget

Deerfield Township’s budget process is very detailed and involves all township staff working with the Finance Department to determine how best to use township funds in the most efficient and effective manner.

Deerfield Township operates on a calendar year budget, meaning the annual budget is passed in December and goes into effect in January of each year.

Below you can find the most recent township budgets.

Annual Comprehensive Financial Report (ACFR)

The Annual Comprehensive Financial Report (ACFR) is the highest level of financial reporting by a governmental organization. The ACFR Program was established by the Governmental Finance Officers Association (GFOA) in 1945 to provide a more comprehensive and detailed illustration of a community’s financial condition.

In the State of Ohio, local governments are required to document what assets they have available and what liabilities they have incurred. Generally, this is accomplished through the preparation of General Purpose Financial Statements. Many governmental organizations have chosen to go above and beyond this process and instead to develop a ACFR. The preparation of a ACFR is totally at the discretion of the community.

Deerfield Township’s ACFR is prepared in-house annually by the Finance Department.

Below you can find a copy of the township’s ACFR from the most recent years.

How Tax Dollars are Spent

Jennifer Richardson, Finance Director

Contact Information

- Phone: 513.701.6969

- Email: jrichardson@deerfieldtwp.com

Experience

Jennifer Richardson currently serves as the Finance Director for Deerfield Township. She is responsible for the financial management of assets, income and expenses for the Township. This includes maintaining the General Ledger, overseeing payroll and preparing all year-end reports for the Township. Prior to joining Deerfield Township in 2006, Jennifer served as the Mortgage Loan Accounting Manager and a Bank Officer for Fifth Third Bank.

Jennifer obtained her Bachelor of Science degree from Xavier University and is currently an active member of the National and the Ohio Chapter of the Government Finance Officers Association.

Understanding Property Taxes in Deerfield Township

Property tax, often referred to as "millage," is calculated based on a property's taxable value. Specifically, it's the amount charged per $1,000 of taxable property value. The County Treasurer's office manages these collected funds, which are then distributed by the County Auditor's office to the various taxing jurisdictions. It's important to note that revenues from specific levies (other than general operating levies) are legally restricted for their stated purposes.

Assessed Value in Ohio: In Ohio, the assessed value of real property—the figure used to calculate taxes—is set at 35% of its estimated true market value. Property assessments are updated annually.

Deerfield Township's Property Tax Collection: Deerfield Township collects property taxes through two main categories:

- Inside Millage: This portion does not require a public vote and is capped at 10 mills under Ohio law. Deerfield Township currently allocates 0.86 mills for general operations and 1.44 mills for Road and Bridge maintenance, totaling 2.30 mills.

- Outside Millage: This portion requires voter approval. The Township's total approved outside millage is 11.80 mills, distributed as follows: 6.80 mills for Fire operations, 4.00 mills for Police operations, and 1.00 mill for Parks and Recreation.

Distribution of Property Tax Revenue: While property taxes are Deerfield Township's most significant and stable revenue source, accounting for approximately 85% of its total revenues, the Township itself receives only a small percentage of the total property taxes paid by its residents. The majority of these taxes are directed to local school districts and various levies imposed by Warren County.

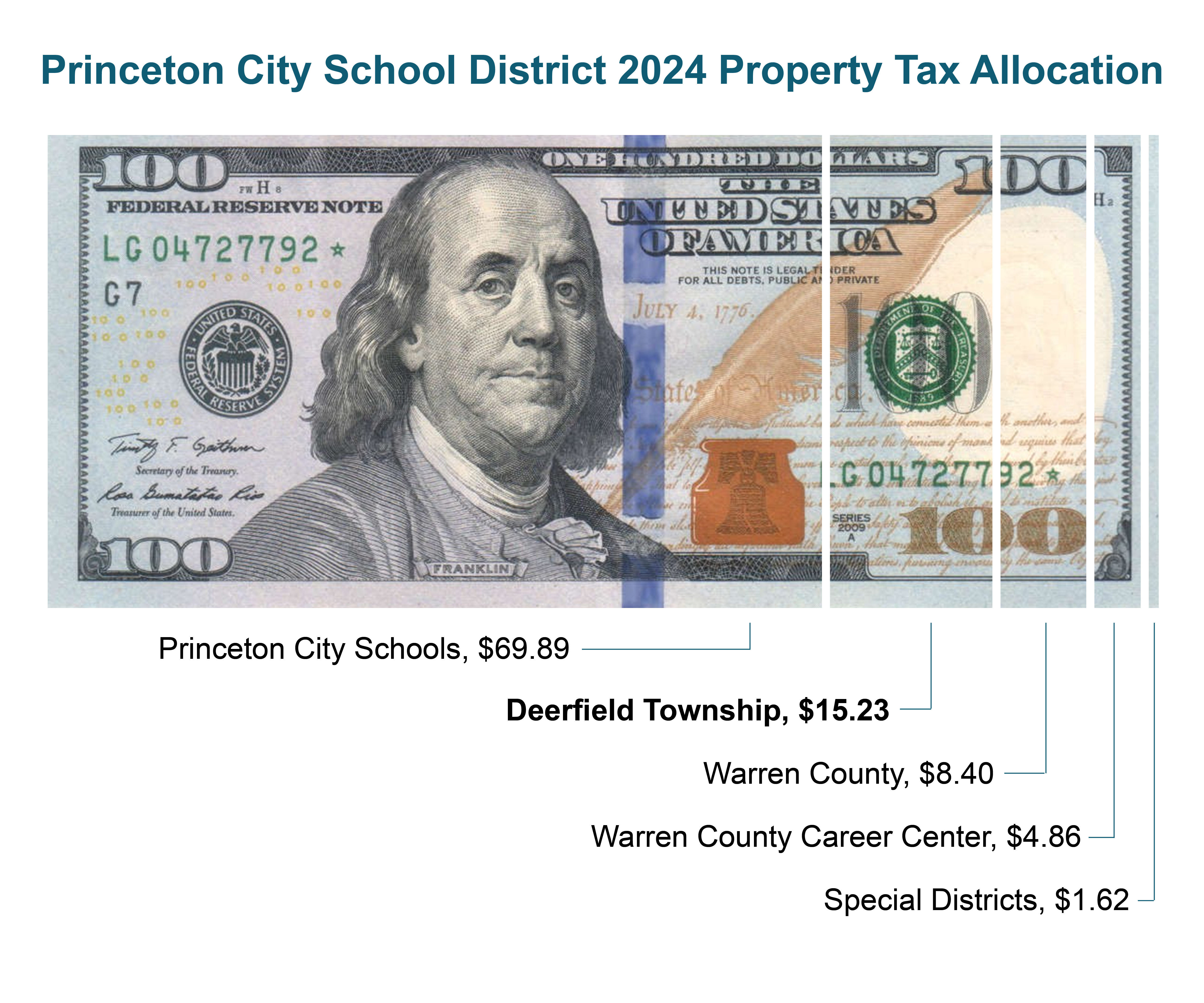

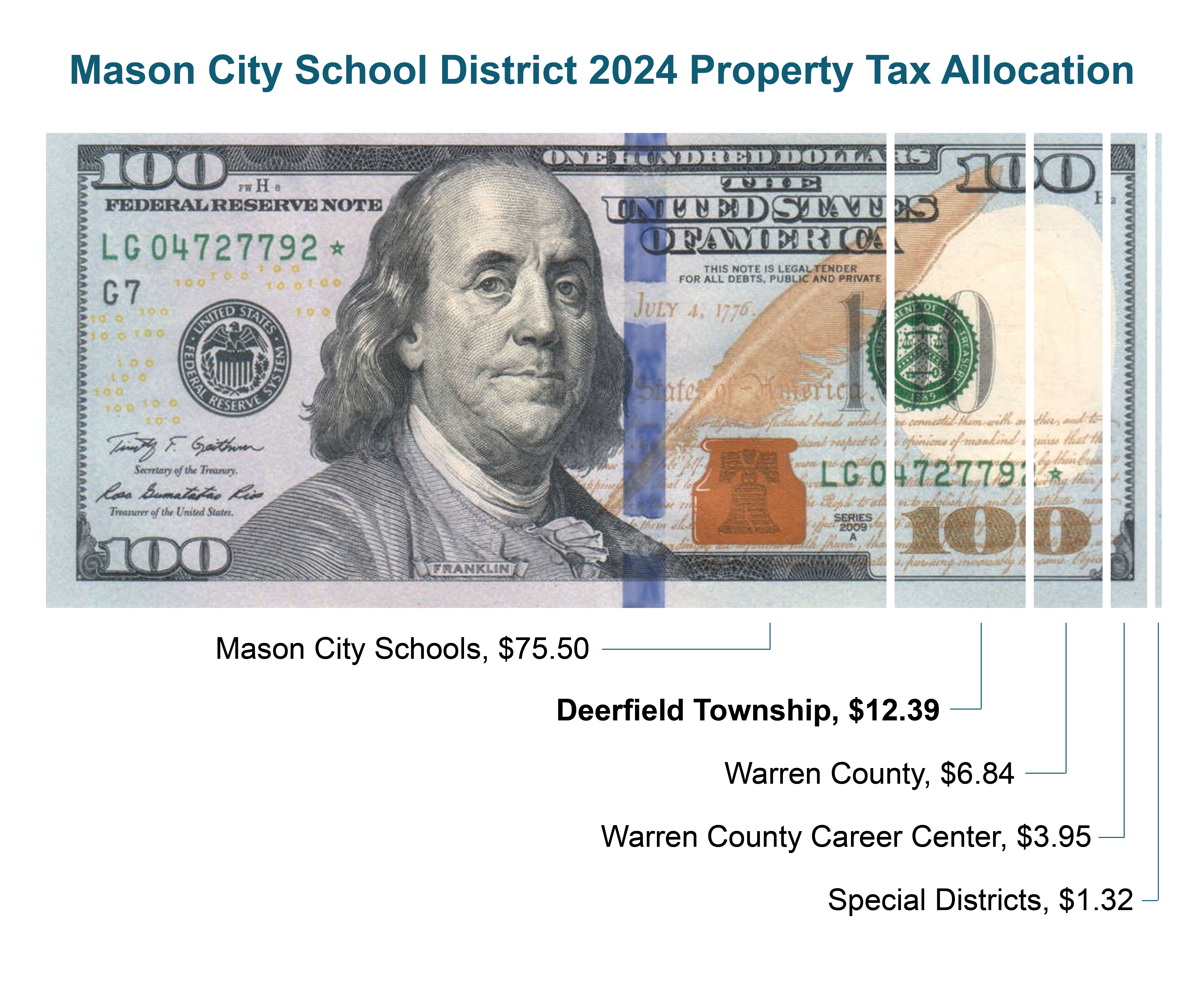

Example Allocation: The following example illustrates how every $100 in property taxes paid on a Deerfield Township home for tax year 2024 (collected in 2025) is allocated. This includes distributions to various school districts such as Mason City School District, Kings Local School District, and Princeton City School District.

Popular Annual Financial Report

You may have heard of a Popular Annual Financial Report (PAFR) and wondered what it is. Simply put, a PAFR is a user-friendly summary of Deerfield Township's financial health and activities. While the Township produces a comprehensive financial report that's very detailed, the PAFR is designed to be much easier for everyone to understand.

What is a PAFR?

Think of the PAFR as a condensed, easy-to-read version of the Township's financial story. It uses clear language, charts, and graphs to show:

- Where your tax dollars come from

- Where your tax dollars go

- The Township's overall financial health

Why is the PAFR Important to You?

The PAFR is incredibly important for Deerfield Township residents because it offers:

- Transparency and Accountability

- Informed Decision-Making

- Community Engagement

In essence, the PAFR empowers you to be a more informed and engaged participant in your local government. It's a vital tool for ensuring our Township remains financially sound and continues to provide the high-quality services we all value.

Jennifer Highfill, Senior Finance Associate

- Phone: 513.701.6961

- Email: jhighfill@deerfieldtwp.com

Stephanie Gebele, Finance Associate

- Phone: 513.701.6960

- Email: sgebe@deerfieldtwp.com

Mason City School District

2024 Tax Property Allocation

Kings Local School District

2024 Property Tax Allocation

Princeton City School District

2024 Property Tax Allocation